It really is a first home buyers’ market

Published 26 Mar 26

A temporary combination of plentiful credit, abundant listings and negligible price growth is benefitting first home buyers.

In real estate speak, it’s a “buyers’ market” right now – but more to the point, is it a first home buyers’ market?

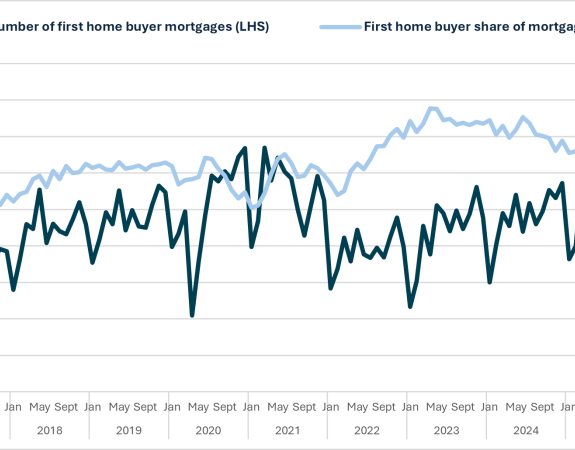

Mortgage lending data from the Reserve Bank shows a steady increase in first home buyer activity since early 2022, when rising interest rates and tighter lending rules slowed borrowing considerably after the 2021 market peak.

December 2025 recorded 3,597 new mortgages to first home buyers, the highest on record, and 7.5% above the previous peak in March 2021. Back then, borrowing was driven by record low interest rates and the temporary suspension of loan to value ratio (LVR) restrictions.

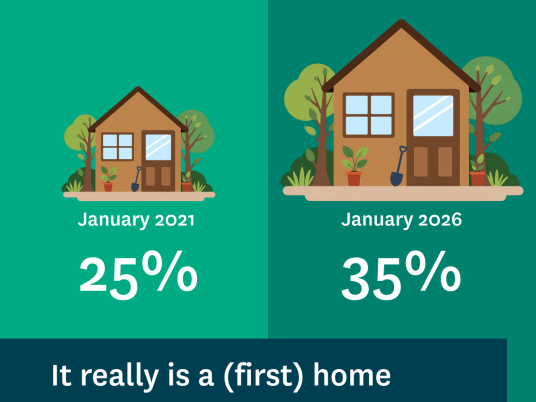

The key difference is who else is in the market. In 2021, strong investor and mover activity meant first home buyers made up just 25% of new mortgages. That rose to almost 40% in mid‑2023, and for most of 2025 has sat around 34%.

So why are first home buyers so active?

First, deposit affordability has improved 11% since December 2023, according to our change in housing affordability dashboard. At the same time, high LVR lending to first home buyers has increased from around 35% in 2023 to roughly 50% today. In other words, nearly half of first home buyers are purchasing without the traditional 20% deposit.

Change in Housing Affordability Indicators

Second, as interest rates have dropped, it has become much easier for people to afford their mortgage repayments – a 70% improvement over the same period. It’s unusual to see deposit affordability and serviceability improving at the same. These factors usually benefit all buyers, but investor activity has remained subdued.

What’s also unusual is the continued high volume of homes for sale. Listings portals are reporting a 10 year high in available stock, giving buyers more choice and removing much of the FOMO that typically characterises housing upswings. That increased activity from first home buyers isn’t translating into higher prices.

For now, first home buyers with the required income to service a mortgage and some deposit saved are in a strong position, both in terms of accessing finance at favourable rates and finding a property that suits.

It really is a (first home) buyers’ market, for now.

Related

-

Data & insight release

It really is a first home buyers’ market

26 March 26

-

Legislation update

New regulations for residential property management sector

24 March 26

-

Publication

Latest renters and landlords pulse surveys – December 2025

22 December 25

-

Legislation update

New regime to protect renters and property owners introduced

18 August 23